Ten Crucial Things You Should Know About Your Utah Business’s Credit Report/Score

To build a strong, resilient foundation for your company, you need to establish good business credit. But how does it work? Our ten tips make it easier.

If you’re a business owner, you might feel overwhelmed by the prospect of building business credit. And much like your personal credit score, it can help or hinder your financial growth. Though it might seem daunting, having a good understanding of business credit and how to build it up over time can open new doors, helping you secure better financing options and positive vendor relationships.

So, what are the most important factors in building a strong business credit score? When does personal credit become a factor?

Here’s everything you need to know:

Setting the Foundation

1. Establish a business identity

1. Establish a business identity

First, you’ll need to register for an Employer Identification Number (EIN). Think of it like a social security number. It’s your first step to making your business official in the eyes of lenders and credit bureaus, and you’ll need it to open a business bank account, file taxes, and apply for credit in your business name.

Next, open a business bank account. It might seem basic, but it’s the most important step for tracking business expenses and showing lenders you’re serious about proper financial management. Your business account will help you make sure all business-related transactions remain separate from your personal expenses, along with maintaining accurate financial records. You won’t be able to build business credit without it.

2. Separate your personal and business finances

Creating clear boundaries between your personal and business accounts is key for building credit and filing your taxes properly. All too often, business owners don’t realize their personal credit score can affect their company until it’s too late. Keeping your business and personal finances separate helps prevent any issues when you’re applying for loans, and it sets the stage for building your credit history.

Q: Does it matter what kind of business structure I use?

A: No. For the purpose of building credit, no one type of business is better than another. You can choose to set it up as an LLC, corporation, or partnership — all are sensible options.

Building Your Credit Profile

3. Register with credit bureaus

Once you’ve set up your business and received an EIN number, you can register with major credit bureaus like Dun & Bradstreet, Experian Business and Equifax Business. These entities will track your payment history, credit, and other factors that influence your business credit score.

Once you’ve set up your business and received an EIN number, you can register with major credit bureaus like Dun & Bradstreet, Experian Business and Equifax Business. These entities will track your payment history, credit, and other factors that influence your business credit score.

Q: Will I receive a score just like with my personal credit?

A: Yes. Companies like Dun & Bradstreet, Experian Business and Equifax Business will give your business a numbered score, though the range is slightly different. Most companies fall somewhere between 120 and 200.

4. Develop a strategy

In order to build credit you’ll need to start using credit with your business. The easiest way is opening a business credit card – but make sure to use it responsibly for company expenses and making payments. If your business is running into problems qualifying for a traditional credit card, you can open a secured credit card based on funds you make available in advance. And when you get your new card, don’t use all of your available credit. Try to keep your credit utilization ratio below 30%. For example, if your card limit is $10,000, keep your balance under $3,000.

5. Maintain good vendor relationships

Whether or not you pay your vendors on time can affect your business credit score, and your ability to secure trade credit in the future. Maintain good working relationships with all of your vendors, especially those that report payments to credit bureaus. When managed responsibly, your vendor relationships can actually help you build credit and establish favorable payment terms.

Best Practices

6. Monitor your credit

Just like with your personal credit score, it’s important to regularly check your business credit reports for accuracy. Errors can happen! And when they do, they can potentially harm your credit score. Check your report with Dun & Bradstreet, Experian Business or Equifax Business on a quarterly basis and immediately file a dispute if you spot any inaccuracies. This kind of regular monitoring and maintenance isn’t just good practice, it also helps you understand how your financial decisions are impacting your score.

Just like with your personal credit score, it’s important to regularly check your business credit reports for accuracy. Errors can happen! And when they do, they can potentially harm your credit score. Check your report with Dun & Bradstreet, Experian Business or Equifax Business on a quarterly basis and immediately file a dispute if you spot any inaccuracies. This kind of regular monitoring and maintenance isn’t just good practice, it also helps you understand how your financial decisions are impacting your score.

Q: Does my personal payment history affect my business credit score?

A: Even after separating your personal and business finances, continue keeping your personal finances in order. When applying for financing as a new business, banks will often ask business owners to guarantee the loan — at which point your personal finances will become a deciding factor.

7. Stay on top of your payments

Your payment history can have a direct impact on your business credit score, which is why you should always make your payments on time. Late payments on loans, credit cards, or vendor invoices can all negatively affect your credit, and potentially damage your business’ ability to secure financing in the future. Many businesses make the mistake of falling behind on payroll tax payments, and penalties can impact your ability to get a loan.

8. Hire a bookkeeper

Proper bookkeeping might be one of the most overlooked practices among small business owners to date. In fact, hiring a good bookkeeper is one of the best decisions you can make. They will ensure that your financial reporting and documentation are completely accurate. Your bookkeeper can also help you file your taxes promptly and correctly. Delays or inaccuracies in your tax filings can result in penalties that may impact your credit score, which a bookkeeper can help you avoid.

Proper bookkeeping might be one of the most overlooked practices among small business owners to date. In fact, hiring a good bookkeeper is one of the best decisions you can make. They will ensure that your financial reporting and documentation are completely accurate. Your bookkeeper can also help you file your taxes promptly and correctly. Delays or inaccuracies in your tax filings can result in penalties that may impact your credit score, which a bookkeeper can help you avoid.

Q: Can’t I just use QuickBooks instead?

A: We get that professional accounting can be expensive, but even the best software can’t replace the insight and experience of a qualified bookkeeper. They can help you keep your business on track, and provide the documentation you need when applying for a credit card or loan.

Strategic Growth

9. Start small and scale

When building business credit, it’s important to only borrow as much as your business can handle. Smaller loans or lines of credit can help you establish a positive payment history, but getting underwater with excessive debt will hurt your business.

As you build trust with your lenders and demonstrate sound financial planning, you can start negotiating larger loans with better terms. By using this gradual approach, you can build a solid credit history without exposing your company to potential risk.

10. Monitor UCC filings

Along with monitoring your business credit score, you’ll want to keep track of your Uniform Commercial Code (UCC) filings. These are liens placed on your business assets by lenders, and they can also impact your ability to secure financing. These liens are typically released when you pay off your loans — but there are rare instances when lenders may forget to remove them. That’s why it’s important to just make sure your UCC filings are up-to-date.

How good credit helps secure last-minute financing

How good credit helps secure last-minute financing

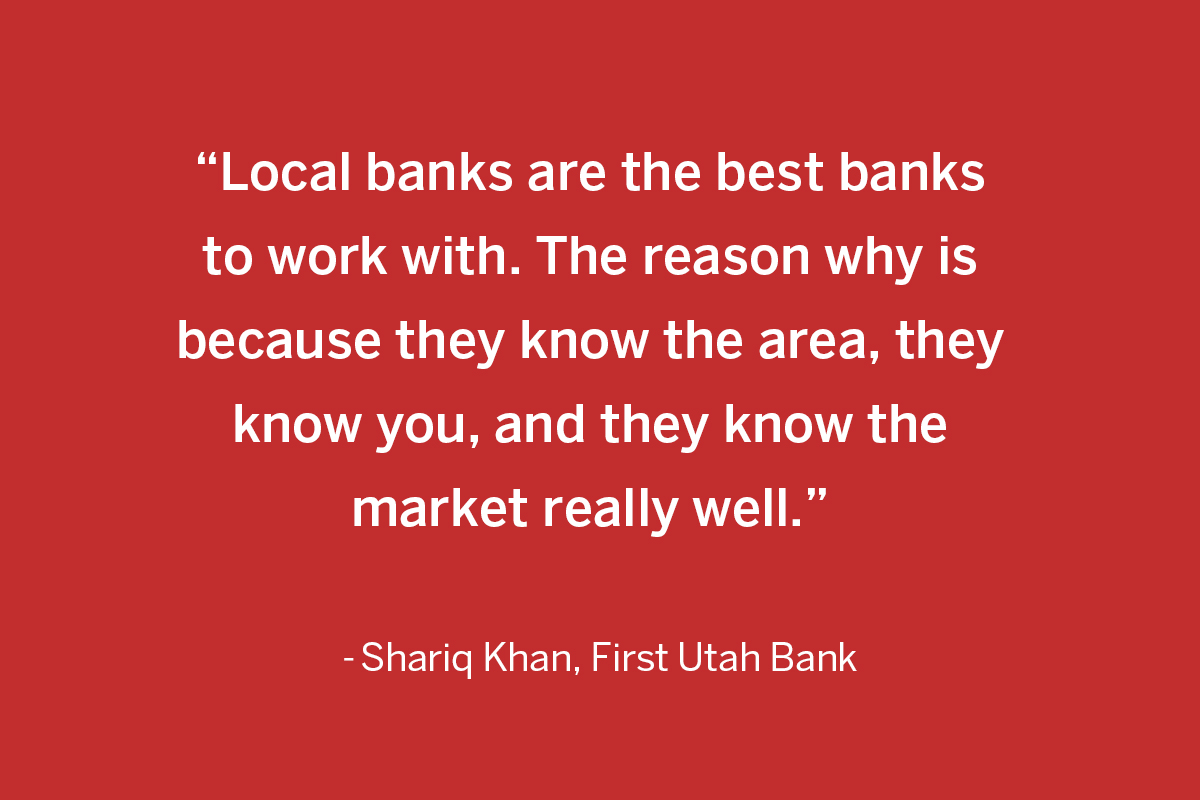

“Here at First Utah Bank, we prioritize our relationships with our customers. Our reputation for service and accessibility is what sets us apart, and it’s what makes us a supportive partner in a time of crisis,” says Shariq Khan, SVP, Credit Department Manager at First Utah Bank.

“During the height of the COVID-19 pandemic, one of our clients needed urgent assistance. A local medical supply business secured a number of large contracts for PPE equipment, but to fulfill their orders they needed quick financing so they could purchase supplies. Thanks to their established relationship with First Utah Bank and solid business credit, we were able to quickly approve some specialized financing so they could move forward with their orders. This is just one example of that small community connection we’re so proud of,” says Khan.

The takeaway: good credit can make or break business opportunities. Developing strong banking relationships can also make all the difference for your company.

Long-Term Success

Building business credit isn’t a sprint — it’s more like a marathon. The time and effort you put in now can create opportunities for better loan terms, stronger vendor relationships, and more financial flexibility when you need it most.

Once you’ve established your business and started building credit, maintaining your books properly is key. Thorough records of your financial statements, tax returns, and payment histories will help you secure financing should the need arise. These documents are necessary for credit applications and to validate your financial performance. They also provide regular insight into your business’s financial health and growth trajectory.

Remember, every successful business started somewhere. But even if you’re building from scratch, there are many ways to build good business credit for a healthy financial future. Doing so can set up your company for success and long-term sustainable growth.

KEY TAKEAWAYS

– Set up a business EIN and bank account

– Consistently use and pay business credit accounts

– Maintain a mix of different credit types (credit cards, lines of credit, vendor accounts)

– Make payments on time

– Keep detailed financial records

– Build relationships with local financial institutions that understand your business

– Regularly review and adjust credit-building strategies